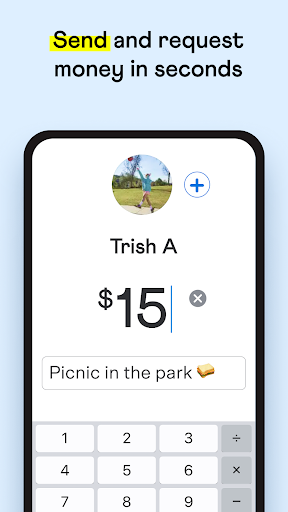

Venmo’s defining feature is that it turned peer-to-peer payments into a social activity. Splitting a dinner bill, paying back rent, settling a group trip — the transactions appear in a social feed with emoji and comments. For its US user base, it became a genuine social norm in the way few fintech products manage. The actual payment mechanics work reliably: linked bank accounts and debit cards transfer quickly, instant transfer to bank is available for a fee.

The social feed defaults to public, which has been a consistent privacy criticism. Sharing financial activity patterns with anyone who looks up your username is a genuine data exposure that many users don’t notice until someone points it out. Venmo has added privacy controls, but the default being public is a product decision that prioritizes network growth over user privacy.

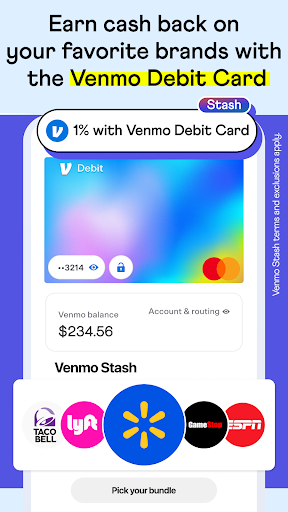

Venmo is now owned by PayPal and the app has grown to include business payments, a Venmo debit card, and crypto features that feel bolted on to a product that was clean as a simple P2P tool. The core still works fine. The expansion has made the app slightly noisier without adding much for the typical use case of paying a friend back.

Verdict: The definitive P2P payment app for its US user base, but the public-by-default social feed is a real privacy concern that users should actively manage.